Africa Deserves Better: My Encounter with a Ponzi Scheme in Disguise

On Friday, 05 September 2025, a LinkedIn post caught my attention with a familiar promise of “financial freedom.” As a creative in the finance space l was curious to know what this was all about. One of the conversations l have with myself constantly when thinking about my finance content curation journey is how do l create content which protects the field as well as protecting the interest of the people.

This particular post had phrases like “remote positions available,” “no experience needed,” and “earn income by helping others” , particularly for audiences in Zimbabwe and South Africa. Out of curiosity, I clicked the link and was added to a WhatsApp group with over 200 people, most with phone numbers from Zimbabwe and South Africa. This particular Zimbabwean named individual claimed to be working with a UK based company (now this might be true or they might be using the company's resources to gain credibility for their scheme they are carrying out.

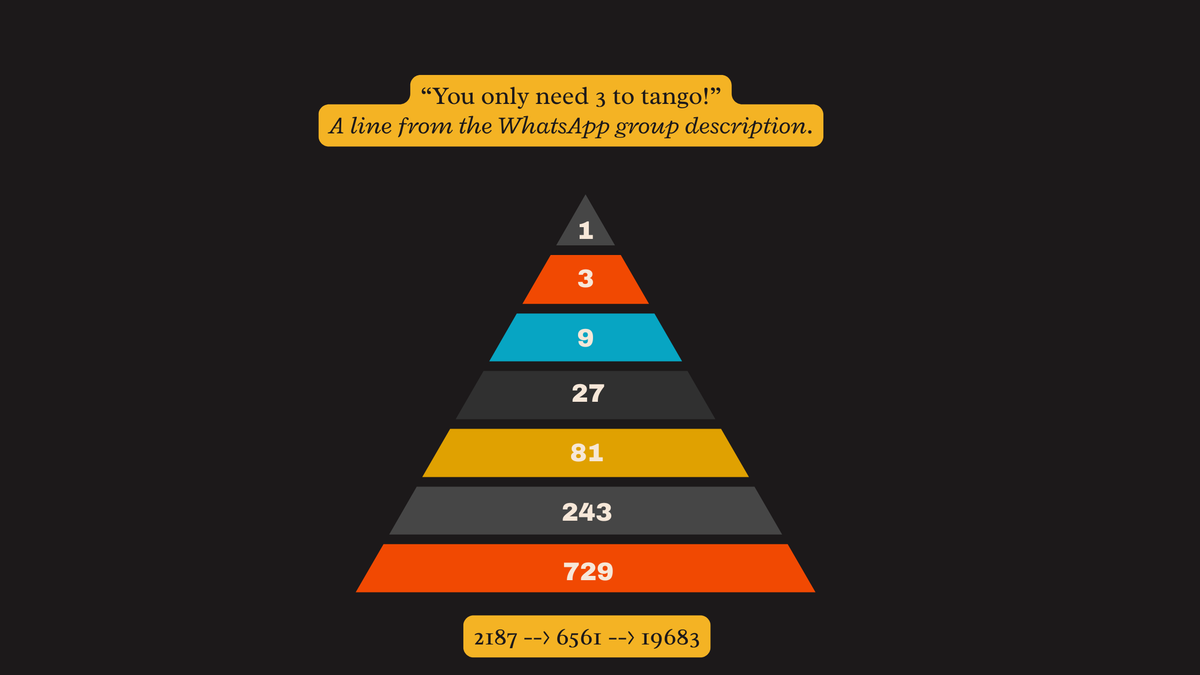

Then I noticed the line from the whatsapp group description:

“You only need 3 to tango!”

That line set off alarm bells. In pyramid or Ponzi schemes, slogans like this are often code: You can only earn money if you recruit more people. To “get paid,” you must bring in new members—usually 2–3 or more—whose contributions fund the people above them. There’s no real product, no genuine service. It’s a cycle where the few at the top benefit while everyone else eventually loses.

The math tells the story: once the scheme tries to pull in thousands (2,187… 6,561… 19,683 at the bottom), it collapses. The recruiters at the base are left with nothing, while the masterminds quietly disappear with the money.

The whole setup felt wrong. The introductory video was vague—selling a dream of wealth without ever explaining how it was created. It was like showing up to a formal event in the wrong clothes. I didn’t belong there.

But this small experience revealed a bigger truth: Africa has become a prime hunting ground for Ponzi and pyramid schemes.

Ponzi schemes aren’t new. The first famous case was Charles Ponzi in 1920 Boston, who promised 50% profit in 45 days using postal reply coupons. He wasn’t generating real returns—he was just paying old investors with new investors’ money. Pyramid schemes go back even further, at least to the 1920s and 1930s, often dressed up as “games” or “clubs.” Over time, they evolved into shady multi-level marketing setups without actual products. The formula is the same: the structure forms a pyramid, the top profits, and the majority lose.

A Continent Repeatedly Targeted

Why does this keep happening here? Because where opportunity is scarce, hope can be weaponized. And with digital platforms, these schemes scale faster than ever.

- Nigeria: The 2016 MMM collapse saw over three million people lose billions of naira after promises of 30% monthly returns. More recently, the CBEX scam stole ₦1.4 trillion—the country’s largest scam to date.

- South Africa: MTI, called the world’s biggest crypto Ponzi, defrauded 100,000 investors across 140 countries, with courts ordering restitution of R32 billion (~US$1.7 billion).

- Zimbabwe: Recent scams include the Morelife scheme (US$197,000 lost), the e-creator scam (nearly US$1 million lost), ABWA Zimbabwe’s collapsed agricultural investment plan, and Beaven Capital’s promise of 50% returns in six weeks—which ended so tragically that one investor took their own life.

These aren’t isolated incidents. They’re patterns. And they’re accelerating.

Why Africa? Why Now?

Africa sits at the intersection of two powerful forces:

- Economic vulnerability – High youth unemployment, unstable currencies, and limited investment options make “fast money” offers tempting.

- Digital connectivity – Platforms like WhatsApp, Telegram, and LinkedIn make it cheap and easy to build large, fake communities that look real.

Scammers also exploit relational trust. They use local names, diaspora links, and foreign company names to break down suspicion. In many places, anything with a “foreign” tag feels more credible. That trust gap is their greatest weapon.

But the damage goes beyond lost money. Families are broken, trust is shattered, and communities fracture. In Nigeria, victims of MMM were driven to suicide. Across the continent, livelihoods are being destroyed.

The Future at Stake

If nothing changes, scams will get even more sophisticated. With AI-generated ads, deepfakes, and hyper-targeted campaigns, spotting fraud will only get harder.

But there is another way forward:

- Financial literacy at scale – Every African should be able to spot a Ponzi within minutes, just as I did when I saw that LinkedIn post.

- Smarter regulation – Regulators need to move faster, leveraging tools like blockchain tracking and AI-driven fraud detection, while also creating free financial education programs.

- Collective responsibility – Communities, leaders, and platforms must speak up. Silence protects scammers. Awareness protects people.

Where Do We Go From Here?

When I exited that WhatsApp group, I carried with me a sense of responsibility. What about the 200+ people who remained? What about the countless others joining similar groups every day?

I chose to write this—not just as a warning, but as a call to action. Through my videos on TikTok, Instagram, YouTube (@rutendofinance), and Facebook (Finance with Rutendo), I am committed to raising awareness and building financial resilience.

But this cannot be a one-person mission. It must be a collective effort. Because what's at stake is not only money—it’s trust, dignity, and the financial future of a continent. Africa deserves better than to be the next hunting ground for global Ponzi schemes. And together, we can make sure of that.